Effect of Interest rates on Real estate - retrospective on UK data since 1964

In my previous posts (link 1, link 2), I wrote that a lot of house price inflation that happened has largely been an effect of interest rates being as low as they are today. In my previous week's post, I also wrote about the connection between interest rates and stock valuations. The natural next chapter, then, is to look at the effect of interest rates on house prices.

In theory

At the basic theory level, interest rates are integral part of the home ownership equation. Given vast majority of home owners borrow to fund the purchase, and that interest rates directly affect the affordability of loans, theory dictates that increasing interest rates must have a dampening effect on demand on property. But by how much?

Is it really that much?

In practice, property market doesn't quite move as much as theory would suggest. This is due to a combination of reasons

- Houses don't transact that fast and hence adjustment in prices don't happen that rapidly.

- Houses being an emotional purchase often end up transaction beyond economic fundamentals, at least within a few percentage points of valuations.

- Changes in interest rates are often not reflected immediately due to in-principal approvals etc, which can last for up to 6 months.

- People's economic buying power also changes with interest rate change (often positively) - i.e. wages go up, deposits grow in time etc; and these act as balances on the other side.

- There is supply flexibility in the market. Most property owners prepare for lack of liquidity. When they don't get the price they desire, they just take the property off the market, which in turn buoys the prices at which transactions happen.

In Practice

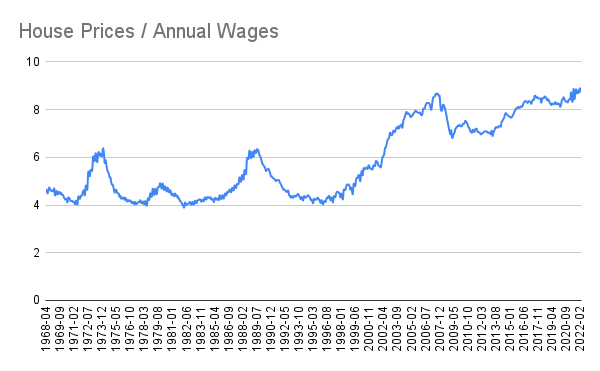

However, when you plot it as a multiple of wages, then things start looking a lot more interesting:

In fact it seems that house prices moved within a range of 4x annual wages to 6x annual wages between 1968 to about 2002. After this there has been a discernible movement of this band to be between 7x annual wages. This makes sense, as women have come into workforce a lot more in the last 20 years, families are typically 2 income owners now compares to the 70s or the 80s, and hence the affordability of homes has gone from being funded by one set of wages to 2 sets of wages.

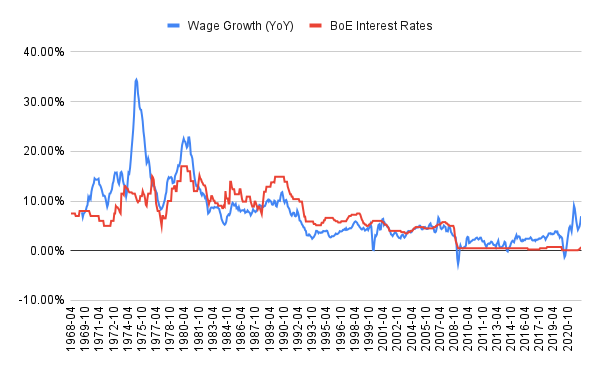

While the correlation isn't 1 to 1, it comes out to be 0.68. This means that when interest rates go up, employees are able to demand and obtain wage improvements that tend to be directionally right. Wage growth also slows down during times of low interest rates. This correlation makes sense - interest rates are often an indication of high levels of economic activity, paired with inflation. So, the high level of economic activity leading to higher wage growth largely makes sense.

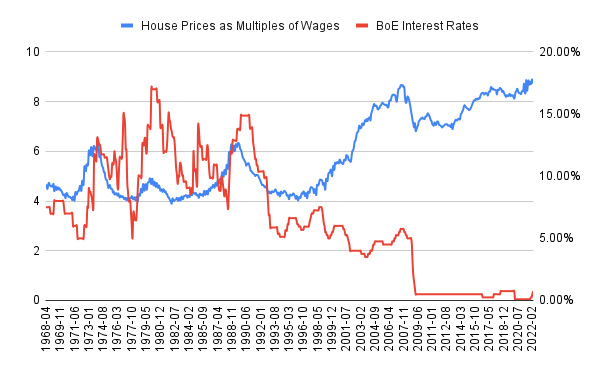

For most of the 54 year data records, it seems that higher the interest rates, lower is the wage-multiple property buyers are willing to pay for houses and vice versa. This graph may not show it as clearly, so I plotted the rate of change of the blue line - i.e wage-multiples, to see if I can see a clearer mirror effect between the two lines and indeed, that seems to be the case:

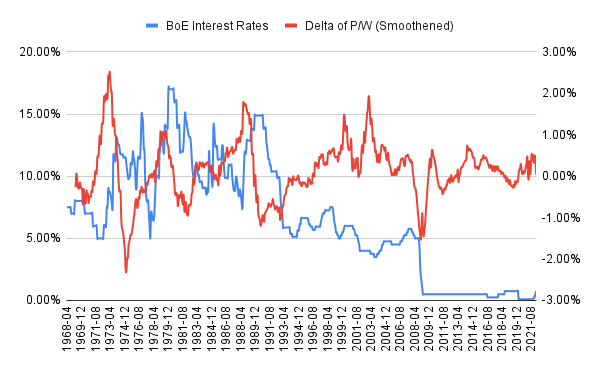

If you carefully observe, in every phase the blue line has gone up, the red line has trended down and vice versa. The correlation between the two is -0.12. Quite not the smoking gun, but directionally observable.

- Theory suggests that property prices should come down when interest rates go up.

- In practice, property market goes through cycles, less on absolute value, than on price-to-annual-wages basis

- When observed in historical data:

- wage growth doesn't get tempered by interest rate hikes, which is good news for the workforce.

- price-to-wage multiples tends to get tempered by interest rates

Comments