Review of UK's tax growth ahead of Autumn Budget

This week we are expecting another budget from another Chancellor in the UK. Ahead of the budget, there has been a lot of kite flying, with promises to look at almost every avenue available at the hands of the government, to fill the purported £50-£55 Bn gap in the fiscal books.

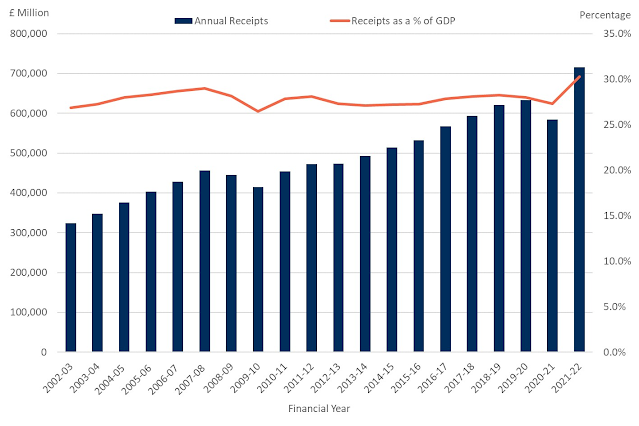

Regardless of the options Jeremy Hunt deploys to solve this problem, let’s take a look at the UK's public finances. Receipts as a percentage of GDP is already nudging 30% with over £716 Billion is collected by the country as taxes, both direct and indirect. Add another £55 Bn, or about 7% more in tax collections, to this and we are talking about taking out another ~2.4% of GDP towards tax collections. That will leave the UK north of 32% - a historical high.

Recently, I wrote about where our household budget gets allocated. That took a look at household finances on a post-tax basis. On a pre-tax basis, for every £100 earned, that represents somewhere around £70 as £30 is taken off the top in the form of income taxes and NI. This is despite the fact that I aggressively employ tax saving mechanisms - primarily through pensions relief. Of the £70 we get in hand, some £22.33 goes towards VATable expenditures, giving the exchequer £3.72 in VAT collections. Of insurance premiums worth £2.87 our household pays in a year, the government collects £0.31 in Insurance Premium Taxes. On SIPP Contributions, roughly £17 in our case, the government has a claim on deferred taxes, which depends on how you withdraw, but can go all the way up to 55% (for those over lifetime allowance). If you take a blended rate of 32%, that’s another £5.44 for each year’s SIPP collections that are due to be collected by the government in the future. If you were somehow lucky enough to put away some money into savings, say £15.47 roughly in our case, then there is capital gains due on it, but not just on gains made this year, but likely of gains from past years. If I were to assume all my past monies add up to roughly 5 times my current year’s savings, and apply a 7% return on capital, that’s £6.50 in capital gains this year, or £1.30 due to the Chancellor’s coffers in form of deferred capital gains. Remember that when you die, you got to give back 40% of your wealth to the government too, and if you were to apportion that at 1% for each year (I am 42 years, and a life expectancy of 82 seems fair to me), that’s an additional £1.10 in taxes owed, again the future.

If you add it all up, the government claims about £43.83 of every £100 that your employer is willing to employ you at, at least for my household. I am certain the calculation is arguable at best, as some of the deferrals and forward taxes are likely overstated, but it is clear that the government is already taking about £40 for every penny entering middle-income households, despite provisions for tax reliefs. If we were to add another 7% to this, that stresses the finances of households that much further.

Comments